Modern pricing systems are vital during a geopolitical crisis that is as volatile and dynamic as this one that is impacting so many different areas of cover, writes Dani Katz, founding director, Optalitix

As I write, a two-week ceasefire has been agreed between the US and Iran, but negotiations appear to have failed as US vice president JD Vance and his team head home.

This war is both a geopolitical shock and a significant insurance market event. It could have significant implications not just for insurance rates but also how global insurance is purchased as governments step in to offer protection.

Underwriters and pricing teams are monitoring events closely.

Since the US-Israeli strikes began on 28 February 2026, retaliatory attacks by Iran and affiliated actors have spread across the Gulf and wider Middle East, hitting ships, ports, and energy assets.

The war has severely affected traffic through the Strait of Hormuz, which has now all but collapsed despite the declaration of a ceasefire.

Affected insurance covers remain available, but at materially higher prices and more selective underwriting. The immediate effect has been a sharp repricing in marine war risks, hull, and cargo.

More broadly, we are seeing a wider hardening across political violence, energy, and trade-related insurance covers in the region.

It is as important as ever for insurers to understand how events could impact their risk.

In this environment, insurers with legacy pricing systems are exposed. Insurers that have digitised their pricing systems are in the driving seat as they adapt to changes faster, and understand their risk exposure in real time.

Material impact on the Strait of Hormuz

Iran has used its control over the Strait of Hormuz as an important tool in its retaliation efforts, effectively constrained passage for most ships.

The waterway remains a central pressure point for global energy and trade generally.

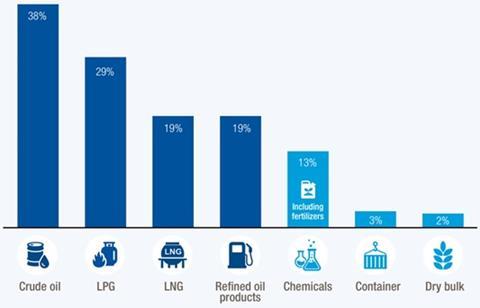

Figure I below shows the share of global seaborne trade volume passing through the Strait one week prior to the conflict.

The 2-week ceasefire offers respite, with no guarantee of a permanent solution. Efforts are underway to reopen the Strait, but the outcome of recent discussions are far from certain, with the most recent negotiations having ended with no further agreement.

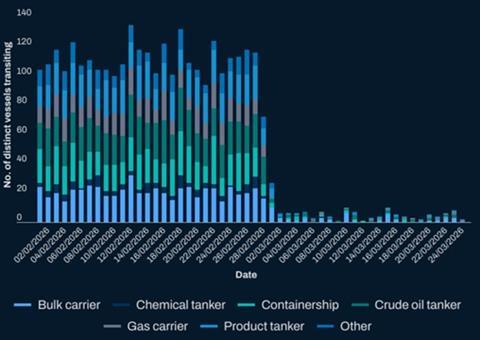

Traffic data clearly shows the scale of disruption. Lloyd’s List reported on 2 March that overall traffic across all sectors through the Strait dropped 38% on the Saturday immediately after the first strikes, with 72 cargo-carrying vessels over 10,000 dwt transiting, versus the normal average of 107 ships per day.

The Lloyd’s Market Association further reported on 23 March that only 111 cargo-carrying vessel transits above 10,000 dwt had been recorded from the start of March to the end of week commencing 16 March, and that ship movements through the Strait were largely sanctioned or shadow fleet tonnage.

At the end of March, Bloomberg ship-tracking data was showing that average March traffic through the Strait had fallen to barely six vessels a day, compared with about 135 in normal conditions.

By late March, more than 80% of transits were shadow fleet or Iran-linked vessels, compared to 12-15% in February.

How Iran is blocking shipping traffic

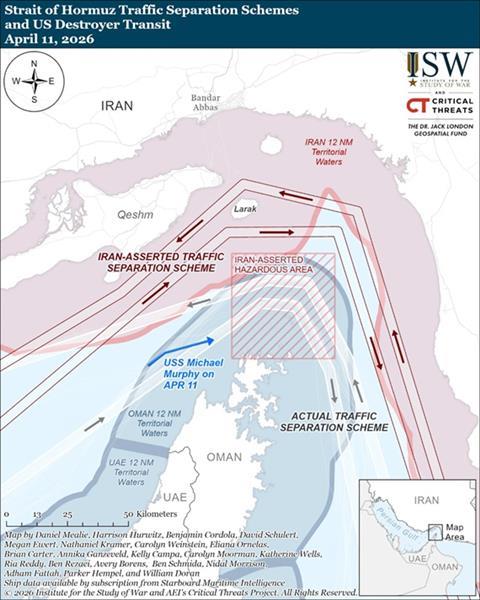

Iran claims it has laid naval mines in the Strait of Hormuz to force ships to use Iranian territorial waters to cross the Strait. This enables Iran to charge a toll while these ships are in Iranian waters. Iran warned ships that the mines could exist in the area marked in the map below as “hazardous water”, forcing ships to go into Iranian territory to cross the strait.

This type of protection racket is illegal under maritime law, and creates legal issues for any companies that pay it due to Iranian sanctions.

At the time of writing, the United States is attempting to undermine Iran’s ability to use the threat of mines in the “hazardous area”.

US Centcom confirmed that the USS Frank E. Peterson and USS Michael Murphy transited the Strait of Hormuz and as part of a broader mission to ensure the strait is fully clear of sea mines previously laid by Iran’s Islamic Revolutionary Guards Corps.

Which insurance rates are being directly affected by events, and how?

· Marine War Risks: This saw the most dramatic impact, with premiums surging (in some cases over 1,000%) from ~0.25% to as high as 3-10% depending on risk exposure. Rates peaked mid-March but began easing later in the month as tensions showed signs of stabilising. Cover remains available, though insurer appetite varies.

· Cargo War Risks: Rates have increased but less sharply than hull war risks. Pricing is now assessed per shipment, with insurers adding restrictions (e.g., route exclusions and short-term cover) to stay flexible. Availability remains relatively strong.

· Marine Hull (non-war): This experienced moderate repricing, with expected increases of 25-50% in the Gulf region. However, a direct attack on commercial shipping could trigger much more significant rate escalation.

The wider regional market is seeing hardening rates in speciality lines. Attacks and disruption have affected Oman, the UAE, Bahrain, Qatar, and Iraq, alongside continued risks to Israel and Lebanon.

Government entry to the insurance market

The US has stepped in as insurance markets have pulled back. They are providing up to $40bn in reinsurance guarantees to encourage shipping through the Strait amid high-risk conflict, covering war risks such as attacks by hostile forces.

Led by Chubb and supported by major insurers including AIG and Berkshire Hathaway, the programme offers specialised political risk coverage through the US International Development Finance Corporation (DFC).

It is important to note that only US insurers and reinsurers can participate.

This is not the first time the government has entered the insurance market. For example, this exists in the US for state-backed property insurers in catastrophe exposed states, and the UK government provides backing for terrorism and flood cover in the UK.

Current reports show that there is little to no uptake on the program. This cover doesn’t help while Iran is effectively blocking the Strait (which they continued to do at the time of writing despite the ceasefire), but it does change the pricing dynamics of the insurance market. Companies that would have approached the traditional insurance providers, such as the London market or Lloyd’s, can now get cover elsewhere, at potentially cheaper prices.

Pricing implications for insurers

Modern pricing systems are vital during a geopolitical crisis that is as volatile and dynamic as this one that is impacting so many different areas of cover.

It is critical for insurers to be able to track the location and routes of insured assets and identify risk exposures in real time when pricing marine insurance.

This isn’t possible using legacy systems – it requires a modern pricing system that is connected to real time data feeds and can provide these insights and guidance on risk appetite to all underwriters in real time.

The US government’s move to provide cover has wider implications for the London Market in particular who play such an active role in reinsuring the most difficult risks globally.

The US is unlikely to replace the experience and size of the London market, but it does mean there is now an alternative.

This has pricing implications at a time when premium rates are already softening, and the London market will be watching closely to see if there is any expansion of this cover.

This concern is clear from the LMA’s published statements on 23 March regarding the availability of cover for vessels operating in the Strait of Hormuz.

Insurers operating in this space are well advised to consider how they are monitoring pricing and managing risk exposure as this crisis unfolds.

By Dani Katz, founding director, Optalitix

No comments yet