Ratings agency gives stable outlook on European insurers, says P&C profitability has recovered and life demand remains strong, but gains are likely to plateau as pricing softens and Middle East risks grow

Moody’s Ratings has maintained a stable outlook for Europe’s property and casualty and life insurance sectors, while warning that intensifying competition and geopolitical instability are creating growing headwinds for profitability.

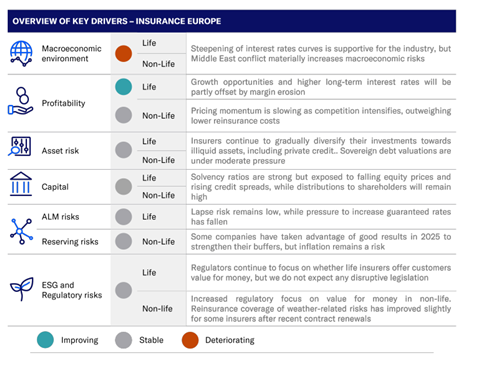

In its latest sector outlook, Moody’s said European P&C insurers had largely restored profitability to pre-COVID levels after pushing through significant price increases to offset inflation and weather-related losses.

However, the ratings agency cautioned that the momentum is beginning to fade.

“Further profitability gains are unlikely as slow economic growth will gradually intensify competition, offsetting lower reinsurance prices,” Moody’s said.

The report noted that combined ratios across major European markets are now at or below pre-pandemic levels, helped by earlier pricing actions.

But pricing momentum in both motor and property insurance is now slowing across many countries, with increases only just keeping pace with claims inflation.

“In the UK, prices have already started to fall, pointing to a deterioration in combined ratios in the months ahead,” the report said.

Moody’s said lower reinsurance pricing should provide some support to primary carriers following recent renewals, with some larger insurers securing broader catastrophe protection than in previous years.

At the same time, the agency warned that its outlook assumes only a “relatively limited impact” from the Middle East conflict.

A more prolonged escalation could trigger market volatility, wider credit spreads, weaker economic growth and renewed inflationary pressure, all of which would weigh on insurers’ solvency and profitability.

On the life side, Moody’s said insurers continue to benefit from strong demand for savings and retirement products, particularly in markets such as the UK and the Netherlands, where pension buyout activity remains robust.

The report also highlighted improving conditions for long-dated savings products as short-term interest rates decline while longer-dated yields rise.

“This will support premium income and reduce policy lapse rates, particularly in France, where competition between banking and insurance products is particularly intense,” Moody’s said.

Nevertheless, the agency expects life insurance margins to narrow as competition intensifies and regulators continue scrutinising whether products provide customers with sufficient value for money.

In the UK, competition for bulk purchase annuity business and the illiquid assets used to back liabilities is already placing pressure on profitability.

Moody’s also expects insurers gradually to increase allocations to private credit and other illiquid assets as they diversify portfolios in search of yield.

At the same time, higher interest rates have continued to support solvency ratios across the sector.

However, the agency warned insurers remain exposed to equity market corrections and widening sovereign or corporate spreads.

Shareholder distributions are also expected to remain elevated.

“Dividends and buybacks accounted for close to 70% of large primary insurers’ profit in 2025, and many insurers now have a progressive dividend policy,” Moody’s added.

No comments yet